Are you considering building your dream home from the ground up or transforming your current home into your ideal living space through renovation? Beyond Broking is here to help you turn those dreams into reality with Construction Loans. These versatile loans are designed to fund construction projects, whether it's building a new home or renovating your existing one. With our expert guidance, you can achieve your home building or renovating dreams more efficiently and affordably than you ever imagined.

Whether you're at the early stages of budgeting and planning or ready to hit hammer to nail, Beyond Broking is your partner during every phase. We're here to guide you, explore your options and turn your home plans into reality as swiftly as possible.

Staged Approach

Funds are released in stages to ensure you are only paying for completed works.

Interest Only

Only pay the interest on your loan until your construction has been completed.

Flexible Repayments

Choose a repayment option that works with your pay cycle.

We provide custom financing solutions to meet the unique needs of your construction or renovation project.

Our experts assist in creating a budget that aligns with your vision and financial capacity, ensuring you stay on track.

We guide you through the loan application process, securing the necessary funds efficiently and cost-effectively.

We leverage our extensive experience and background in accounting and finance, along with a vast network of industry connections, to provide clients with unparalleled insights, resources, and support throughout their construction or renovation journey.

Beyond Broking is committed to your satisfaction, ensuring your construction or renovation project exceeds your expectations.

We work efficiently to expedite the loan approval process, so you can start building or renovating your home as soon as possible.

Construction Loans are specifically designed to provide the necessary financial support for individuals looking to build a brand-new home tailored to their unique specifications.

This financing option is available to both potential homeowners and investors who aspire to construct a residential property. Whether you're planning to build your dream family home or an investment property, Construction Loans can help you achieve your goals.

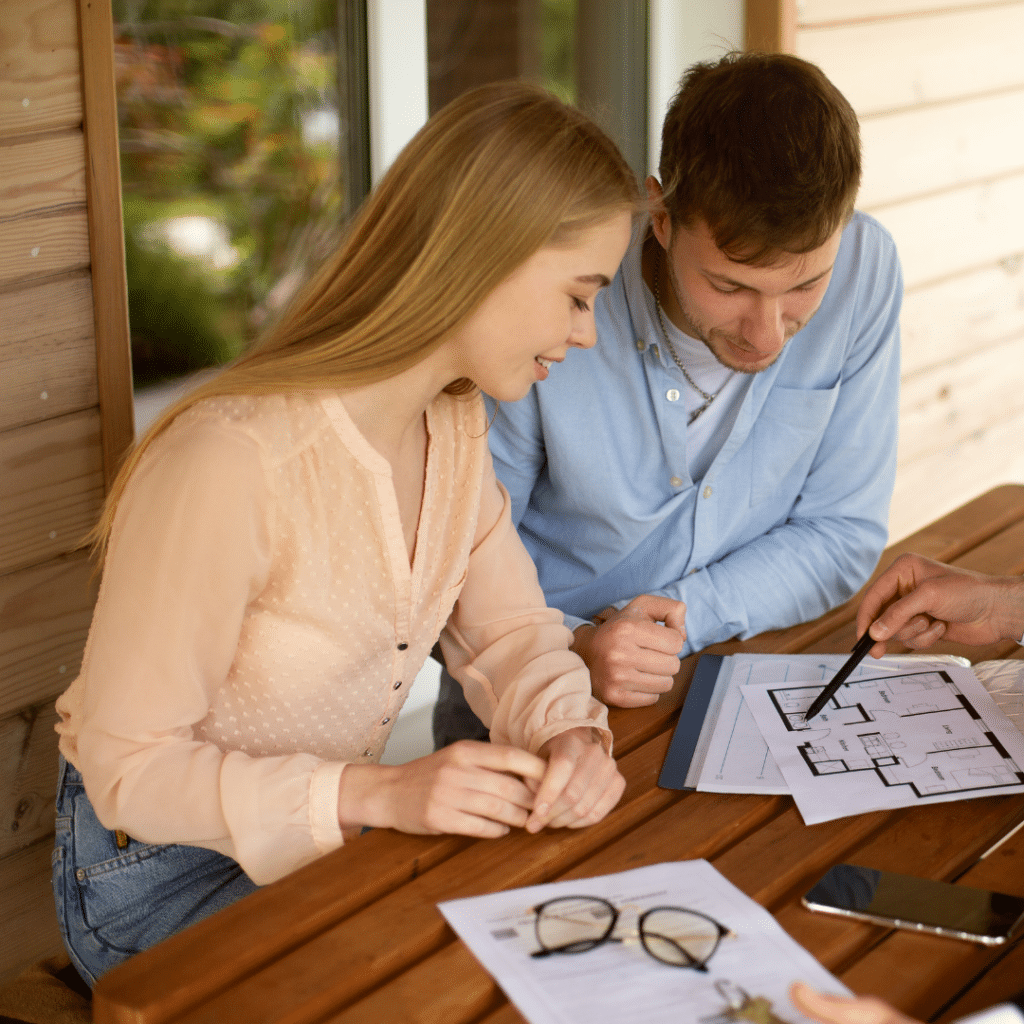

Initial Consultation: Begin by sharing your vision with Beyond Broking during a complimentary consultation. Our team assesses your financial situation to ensure your construction plans align with your budget.

Budget Planning: Collaborate with our experts to create a comprehensive budget, considering construction costs, permits, contingencies, and financial factors.

Loan Application: Beyond Broking guides you through the loan application process, securing the necessary funds for your project's financial component.

Construction Phases: Once your loan is approved, funds are released in approximately 5 - 6 stages to reflect construction milestones. Your building contract should detail your progress payment schedule.

Final Handover: This final stage in the construction journey signifies when you officially take ownership of the house and make the final payment to your builder.

Construction Loans provided by Beyond Broking offer you the financial backing and guidance needed to turn your dream home into a reality. Whether it's your first family home or an investment property, we're here to make your construction journey a smooth and rewarding experience.

Renovation Loans are tailored financial solutions designed for individuals looking to breathe new life into their existing homes. Whether you're planning a minor update, such as a kitchen remodel, or embarking on a major overhaul, these loans provide the necessary funds to turn your renovation dreams into reality.

Renovation Loans are accessible to homeowners who are eager to enhance their current properties. This versatile financing option caters to a wide range of renovation projects, from simple cosmetic changes to more extensive structural and design transformations. Eligibility is based on your ownership of the property and your ability to repay the loan.

Initial Consultation: Share your renovation goals with Beyond Broking. We'll assess your current home, renovation plans and budget.

Budget and Design: Collaborate on a renovation budget and design that aligns with your vision and financial capacity.

Loan Application: We'll guide you through the loan application process, securing funds for your renovation project.

Project Commencement: With financing in place, your renovation project can commence according to the agreed-upon timeline.

Regular Progress Checks: Beyond Broking may conduct progress checks to ensure your renovation is on track.

Completion and Enjoyment: Once the renovation is finished and final payments are made, you can enjoy your refreshed and revitalised living space.

With our extensive experience in the field, we at Beyond Broking are well-equipped to turn your renovation dreams into reality. We have a vast network of over 50 lenders, allowing us to analyse and identify the most suitable financial options to fund your project. Our commitment is to provide you with a seamless finance process, ensuring that your renovation journey is as smooth as possible. Contact us today to discover how our expertise can make your renovation loan a reality. Let us be your trusted partner in achieving your home improvement goals.

Loan Application: Much like with any loan, we take time to learn about you, your financial circumstances and your construction goals to understand how much you can borrow.

Loan Assessment & Valuation: A ‘Tentative on Completion’ valuation will be arranged to determine the projected value of your property post-construction or renovation.

Building Contract: Once signed, this must be sent to the lender to get full approval of your construction loan.

Letter Of Offer: Upon approval of your construction loan, you will receive a Letter Of Offer, which you will need to sign. This Letter Of Offer is valid for six months from the date of issue.

Beyond Broking is your trusted partner in the journey towards your dream home, and here to help you navigate these requirements to ensure a smooth and straightforward process. Our expertise in Construction Loans, coupled with our commitment to your financial goals, ensures a smoother and more successful construction or renovation experience.

A construction loan provides funds to build a new property from the ground up, while a renovation loan is used to update or enhance an existing property. Construction loans are for new builds, while renovation loans are for remodelling or renovating existing structures.

Assess the scope of your project and create a detailed budget. Consider construction or renovation costs, permits, contingency funds, and other expenses. Consulting with a financial expert or loan specialist, such as Beyond Broking, can also help you determine the appropriate loan amount.

Interest rates can vary based on factors such as your credit score, loan type, and lender. The interest rate for construction and renovation loans will not be dissimilar to a standard home loan rate, given your financial situation and available deposit is the same. Beyond Broking has access to over 50 lenders, maximising choice and competitiveness for our clients.

Beyond Broking's specialised team works closely with you to ensure you meet eligibility criteria. Our expertise helps you navigate the qualification process, considering factors such as credit history, income stability and project details. We offer complimentary consultations to determine whether you qualify for a construction or renovation loan.

Beyond Broking's specialised financing offers flexibility and guidance at all stages of your project. Our expertise ensures that your construction or renovation venture proceeds smoothly, adds value to your property, and maximises your financial advantages, including potential tax deductions.