Embarking on the journey to homeownership is an exciting journey, but comes many financial considerations, including your house deposit. In this article, we unfold everything you need to know to be able to answer "How much do you need for a house deposit?" and explore various avenues that can help you secure your dream home.

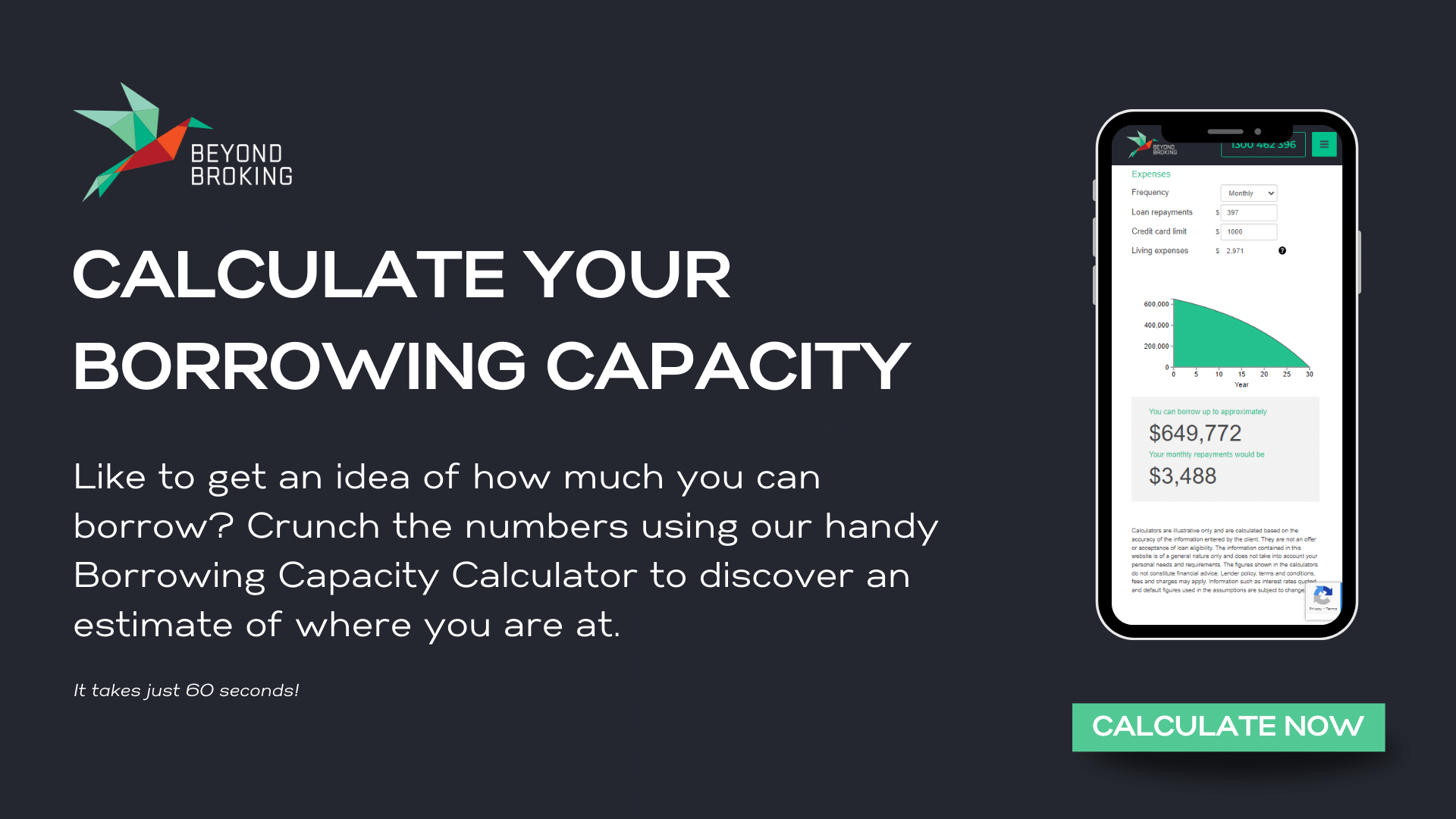

Before setting out on your homeownership journey, precision is key. Utilise our simple online calculator to estimate the required deposit you would need to purchase your dream property. This tool factors in your income, expenses and current interest rates, offering you a good starting point. For a more thorough estimate, book a complimentary consultation with our team.

Navigating the housing market is made more accessible by government initiatives such as the First Home Guarantee Scheme. This program enables eligible first home buyers to secure a property with a deposit as low as 5%, a significant reduction compared to the traditional 20%. To illustrate the impact, consider a property valued at $500,000. A traditional 20% deposit would amount to $100,000, a daunting sum for many. However, under the First Home Guarantee Scheme, the required deposit drops to $25,000, making homeownership significantly more accessible.

The scheme aims to bridge the gap for individuals and families facing financial constraints, ensuring that the dream of homeownership is not limited by the burden of a hefty deposit. The First Home Guarantee Scheme offers a range of benefits that make it an attractive option for first-time buyers. The reduced deposit requirement allows individuals to enter the property market sooner, avoiding prolonged periods of saving and delayed homeownership for those who do not have a 20% deposit.

If the First Home Guarantee Scheme has caught your attention, or if you're curious to see if you qualify, don't hesitate to reach out. Our team of experts has successfully assisted numerous home buyers in accessing this scheme, and we're here to guide you through the process.

For those seeking alternative avenues, leveraging a guarantor can be a game-changer when it comes to your home loan deposit. Typically a family member, a guarantor supports your home loan application, allowing you to secure a loan with a smaller deposit or, in some cases, no deposit at all. Speak to your broker to learn more about this approach and if it is right for you, as a guarantor may be the key to unlocking homeownership for you.

Across various states and territories, the First Home Owners Grant (FHOG) acts as a financial boost for first-time buyers. Learn how to strategically utilise the FHOG to augment your deposit and potentially decrease the amount you need to save independently. This grant might just be the momentum you need to kickstart your journey towards homeownership.

Embarking on the savings journey demands strategic planning and disciplined financial habits. If you’re dreaming of owning your own home, it pays to speak with a broker specialising in first home buyer loans, who can help you determine just how much you need to save. Explore practical tips on budgeting, identifying unnecessary expenses, and creating additional income streams to expedite your savings. By implementing these strategies, you'll find yourself on the fast track to accumulating the funds needed to secure your dream home.

Should you have further enquiries or require personalised guidance, do not hesitate to reach out. Our team of experts is committed to helping you navigate the complexities of the property market and assisting you in achieving your homeownership goals. Book a complimentary consultation with our team and take the next step towards your dream home.